Weekly Market Commentary – 10/6/2023

-Darren Leavitt, CFA

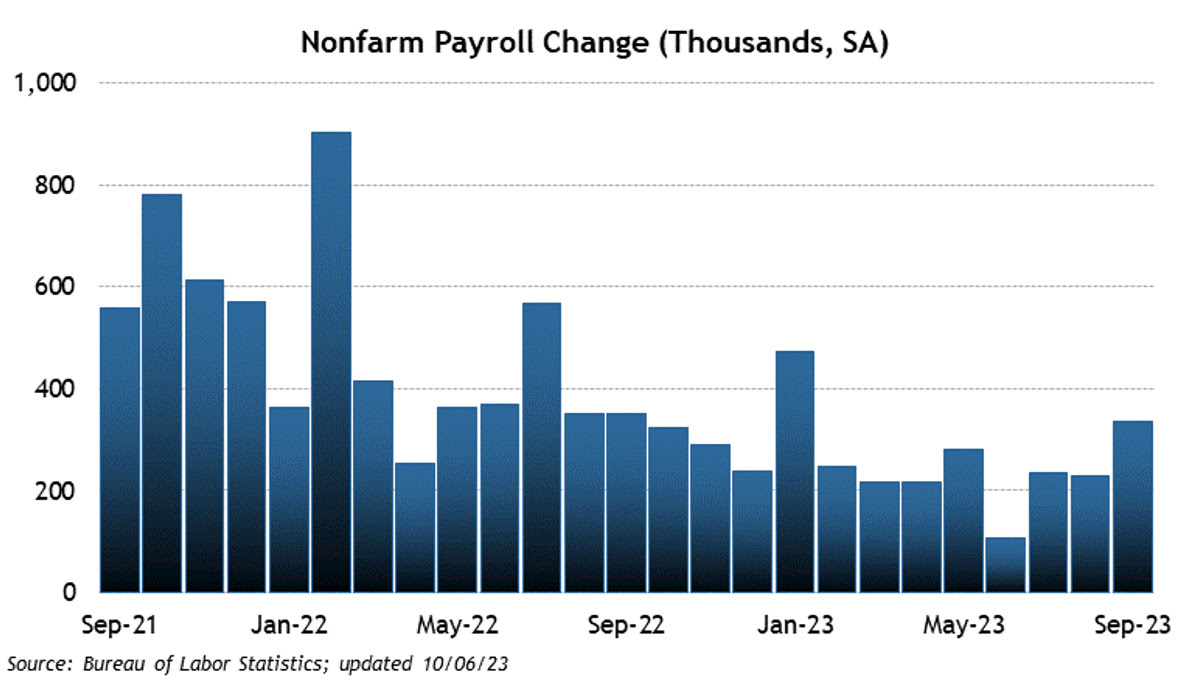

Investors were treated to another mixed bag of market action as the yield curve steepened on the notion of higher rates for longer. There were several central bank officials that echoed the need to perhaps raise rates another 25 basis points and then keep rates elevated through much of next year. A surprisingly strong Employment Situation report propelled the idea of a soft landing, although many think the robust report will mark a top in employment. Fed Funds futures now assign a 42.6% probability of another twenty-five-basis point rate hike by December of 2023. Oil prices plunged 8.12% on concerns over global growth. The move in oil prices came despite Russia and Saudi confirming they would not change their current levels of production.

As I write, there is increased conflict in Israel and the Gaza Strip. Israeli Prime Minister, Netanyahu, has declared his nation is at war. The renewed conflict will without a doubt influence markets as Asia opens Sunday night. US politics continues to be just crazy with the ousting of Speaker of the House this week in a 216 to 210 vote. Republicans are now seeking another speaker who can lead a divided party.

The S&P 500 rose by 0.5%, the Dow gave up 0.3%, the NASDAQ increased by 1.6%, and the Russell 2000 lagged with a loss of 2.2%. The yield curve continued to be sold with longer-tenured Treasuries taking the brunt of the sell-off. The 2-year yield increased by two basis points to 5.06%, while the 10-year yield jumped twenty basis points to 4.78%. The 2-10 spread compressed to twenty-eight basis points. As I mentioned earlier, Oil prices plunged more than 8% or $7.38 with WTI closing at $83.04 a barrel. Gold prices fell $22 to close at $1845.10 an OZ. Copper prices declined by $0.09 to $3.64 a Lb. The US Dollar declined slightly from the most recent highs as the Bank of Japan intervened to ward off more weakness in the Yen.

There was plenty of economic news to digest over the week. The September Employment situation report showed blowout payroll numbers. Non-farm payrolls increased by 336k well above the consensus estimate of 158K and had the prior two readings revised higher. Private Payrolls rose by 263k also well above the consensus estimate. The Unemployment rate stayed at 3.8%, slightly above the estimated 3.7%. Average Hourly earnings increased by 0.2% versus expectations of 0.3%. Average Hours per work week came in line with the consensus at 34.4. Similarly, the JOLTS data showed an increase in jobs at 9.610M from the prior month’s 8.920M. ADP Employment change ticked lower to 89k from 150k. Initial claims came in at 207k and Continuing Claims fell 10k to 1.644M. ISM Manufacturing continued to signal contraction but at a slower pace at 49. ISM Services fell to 53.6 from 54.6 but still showed the services side of the economy in expansion. This week we will see CPI data and PPI data. Investors will also be interested to see the results of 3-year, 10-year, and 30-year Treasury auctions.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involve risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.