-Darren Leavitt, CFA

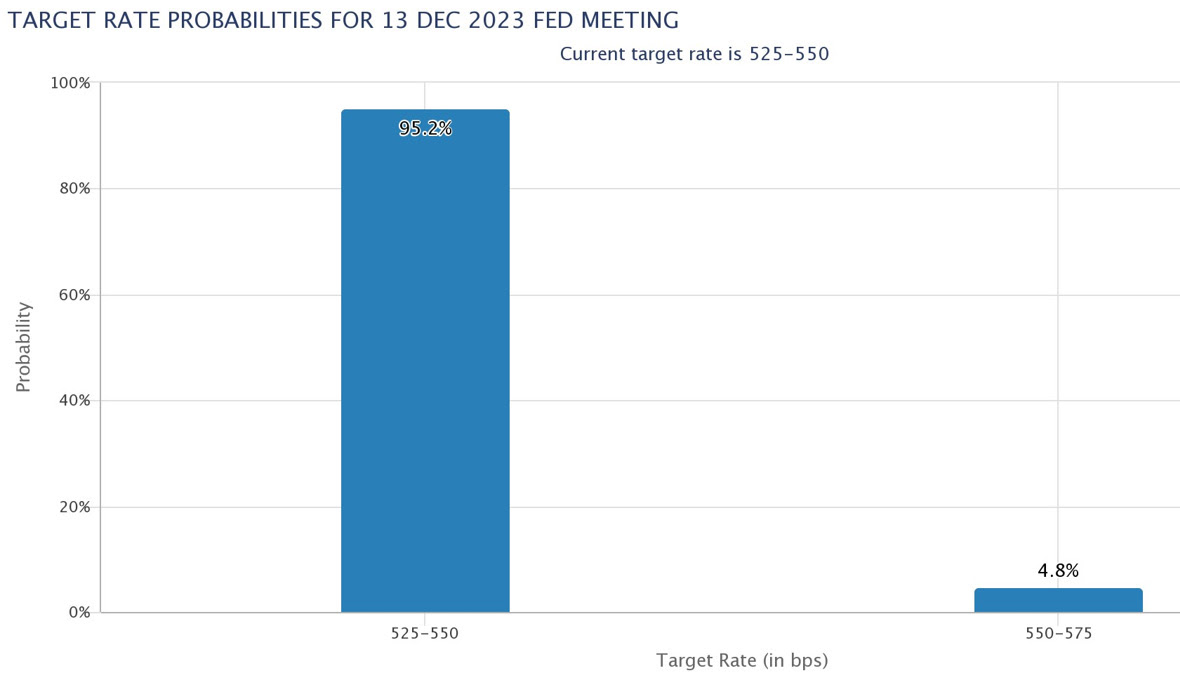

Global financial markets rallied big time last week on dovish tones from central bankers and on the notion that this interest rate hike cycle may be over. The Bank of Japan kicked the week off with a vague move that sets their 10-year Japanese Government Bonds to a target range. The move was less than the street expected and catalyzed the selling of the Yen and jump-started a rally in US Treasuries. The Bank of England left its policy rate unchanged, but three BOE officials voted to increase it by twenty-five basis points. As expected, the Federal Reserve left its policy rate at 5.25%- 5.50%. A more dovish Jerome Powell explained that the Fed had come a long way and that the current policy rate was doing its job in tightening financial conditions. Fed Funds futures indicate that there are no more rate hikes expected this year and signal a couple of rate cuts by the end of next year.

Third-quarter earnings continued to roll and on the margin helped market sentiment. Apple’s earnings were a bit of a disappointment but markets shrugged the tepid results off and moved the market higher. Coming into the week the S&P 500 had been in a technical correction (off just over 10% from the July highs). This week saw massive gains that led the S&P 500 back above its 200-day moving average and above its 50-day moving average. Investors will now wait and see if the market can hold these levels and move higher.

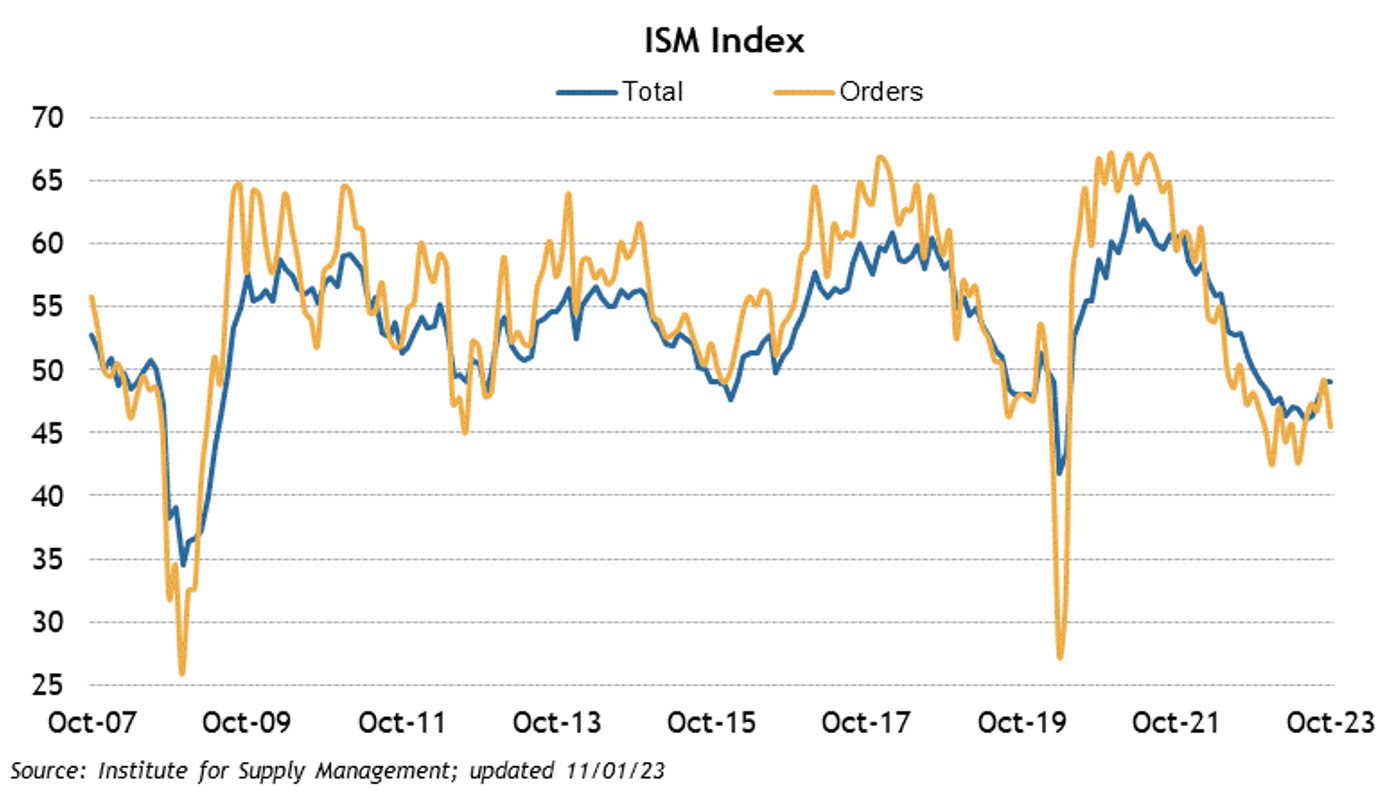

Economic data for the week included the Employment situation reports that showed fewer jobs created than expected. Non-farm Payrolls increased by 150K versus the consensus estimate of 175k. Private Payrolls increased by 99k versus the estimated 143k. The Unemployment rate increased to 3.9% from 3.8% and Average Hourly earnings grew by 0.2%, which was lower than the expected 0.3%. The weaker data helped foster the idea that the Fed is done raising rates. Initial Jobless claims ticked higher as did Continuing Claims. 3rd quarter Unit Labor Cost came in lower than expected at -0.8% while Q3 productivity surged by 4.7%. ISM Manufacturing showed a further deceleration of manufacturing. The ISM came in at 46.7, down from the prior reading of 49.

The S&P 500 gained 5.9%, the Dow jumped 5.1%, the NASDAQ inked a 6.6% advance, and the Russell 2000 increased by 7.6%. The massive upside move in equities was fueled by an equally impressive move in US Treasuries. The 2-year yield fell seventeen basis points to 4.86%, while the 10-year yield fell by twenty-nine basis points to close at 4.56%. The move in rates hindered the US dollar, which fell by 1.4% on the week. Oil prices traded lower by 5.6% or $4.75 to close at $80.78 a barrel. Copper prices increased by 0.04 to $3.68 a Lb. Bitcoin continued its recent advance closing north of $35,000 a coin.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involve risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.